Warning: Late repayment can cause you serious money problems. For help, go to moneyhelper.org.uk. We are a broker, NOT a lender.

Warning: Late repayment can cause you serious money problems. For help, go to moneyhelper.org.uk. We are a broker, NOT a lender.

If you feel a credit broker has charged you unfairly, misled you, shared your details without proper consent, or failed to explain what service you were actually signing up for, it is important to act quickly and clearly. A well made complaint gives the broker a chance to put things right and creates a clear record if you later need to escalate the matter.

This topic also links closely to a common search question: what is a credit broker? Many people only realise they were dealing with a broker, rather than a direct lender, after a fee has been taken or their details have been passed on. In the UK, authorised firms must have a complaints process, and consumers can usually take unresolved complaints to the Financial Ombudsman Service.

A credit broker is a business that helps arrange credit by matching or introducing you to a lender, rather than lending the money itself. The Financial Ombudsman says brokers must make it clear that they are a broker and not a lender, while Citizens Advice explains that they must also set out important fee information in writing before charging in many consumer credit cases.

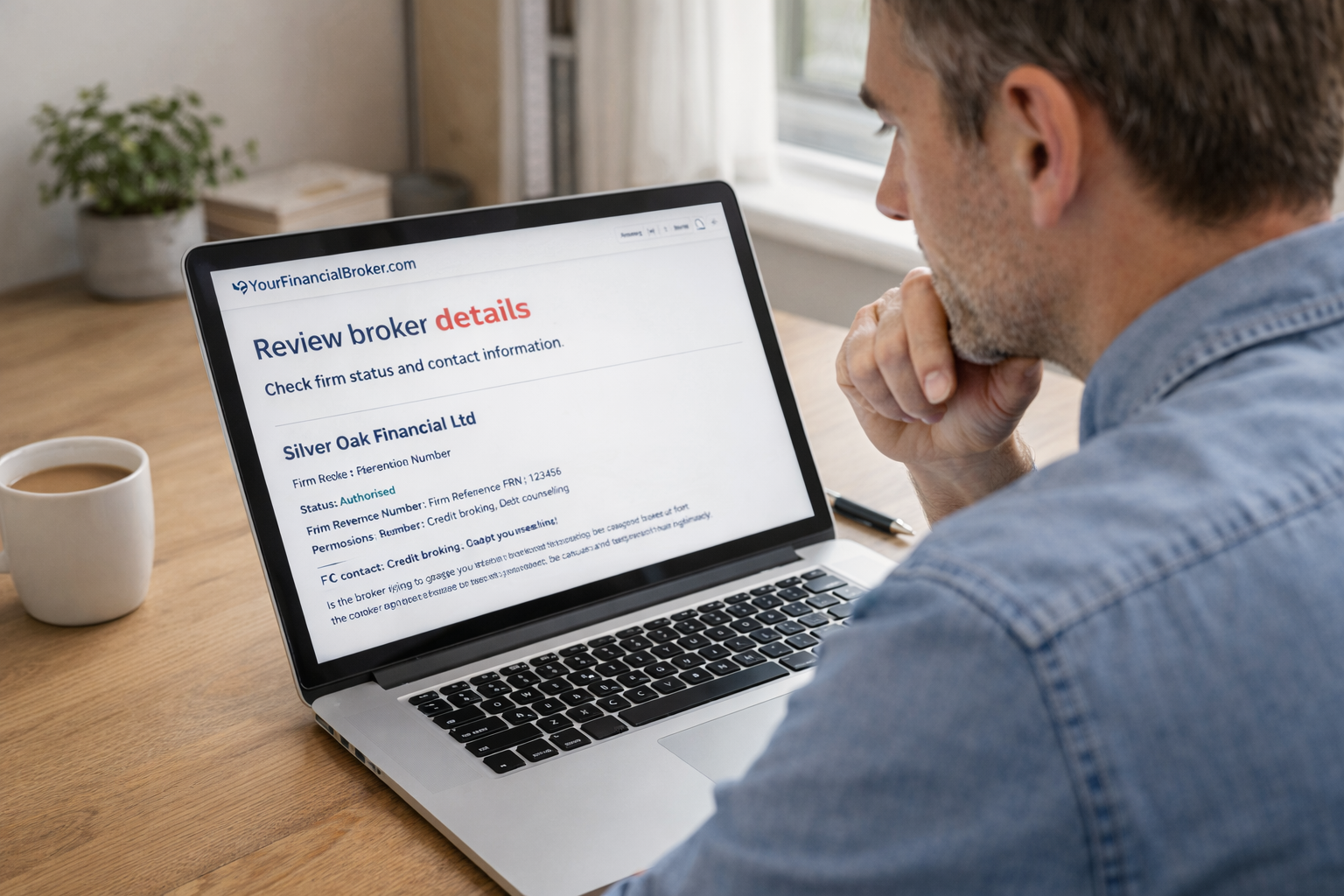

If you have searched what is a credit broker UK, the short answer is that a broker sits between the customer and the lender. Some brokers search a panel of lenders. Others pass your application details on to third parties. That is why it is so important to read the wording on the site, check whether the firm is authorised on the Financial Services Register, and keep copies of what you were shown when you applied.

You may have grounds to complain if a broker:

charged a fee you did not understand or clearly agree to

made it sound like it was the lender when it was actually acting as a broker

took payment even though you did not go ahead with a loan

passed your details to other companies without proper consent

failed to explain key terms, fees, or what service was being provided

The Financial Ombudsman says common credit broking complaints include customers not realising a fee would be charged, being charged even though no suitable loan was taken, or fees being taken too early. Citizens Advice also notes that if a broker has taken payment details without following the rules, or shared personal details in ways you did not agree to, you may be able to complain and seek your money back.

Before you contact the broker, collect everything that shows what happened. This can include screenshots of the website, copies of emails or texts, your bank statement, any information notice about fees, and notes of phone calls. It also helps to write a short timeline covering when you applied, what you believed you were signing up for, what was charged, and what outcome you want.

This step matters because both firms and the Ombudsman will look closely at what was explained to you and whether you agreed to it. The Ombudsman says it checks whether the broker made clear whether it was a broker or lender, what fees applied, and whether your details might be passed to other companies. National Debtline also advises setting out the facts clearly, saying what you are unhappy with, and including evidence that supports your complaint.

Your first complaint should normally go directly to the broker. The FCA’s guide on how to complain says authorised firms must have a complaints process and should be given the chance to put things right. The FCA also recommends making a record of how and when you got in touch.

You do not need legal language. Keep it simple and direct. Explain what happened, why you think the broker acted unfairly, and what resolution you want. That could be a refund, correction of records, removal of charges, or an explanation of how your details were used.

Money problems often get worse when complaints are made by phone only, because there is less evidence. That is why it is usually smarter to complain in writing by email, web form, or letter. National Debtline’s guide to complaining about your lender also recommends putting the complaint clearly in writing and stating what outcome you want.

Timing matters. The FCA says you normally need to complain within six years of the problem happening, or if later, within three years of when you became aware that you had cause to complain. For most complaints, the firm should provide its written outcome within eight weeks.

If the broker sends a final response and you still are not satisfied, or if eight weeks pass without a final response, you can usually take the complaint to the Ombudsman. The Financial Ombudsman Service complaint guide explains that consumers normally need to bring the case within six months of the firm’s final response.

If the broker rejects your complaint, offers too little, or fails to respond in time, the next step is usually the Ombudsman. The service is free for consumers and can look at disputes between customers and regulated financial businesses, including credit brokers. The Financial Ombudsman’s credit broking page explains the kinds of complaints it sees and what information it considers.

This is often where people get results, especially where fees were not properly disclosed, the firm created the impression that it was a lender, or personal data was used in ways the customer did not understand. If the Ombudsman decides in your favour and you accept the decision, the firm must comply.

If a credit broker took an unauthorised payment, do not limit yourself to complaining only to the broker. Citizens Advice says your bank may also be able to help you recover the money, and that raising the matter with your bank does not stop you also complaining to the Ombudsman. This can be especially important where card details were passed on or charges were taken without proper permission.

If the facts suggest fraud or a scam rather than poor service, you may also need to report the issue separately and act quickly to secure your account. Citizens Advice warns that certain fee demands and payment methods can be signs of a scam.

A good complaint is clear about the remedy you want. Depending on the case, you might ask for:

a full refund of the broker fee

a refund of any related bank charges

written confirmation that your details will not be shared further

correction of inaccurate records

compensation for distress and inconvenience where appropriate

The Ombudsman says the aim is usually to put you back in the position you would have been in if things had not gone wrong. In some fee disputes, that can mean telling the broker to refund all or part of the fee, especially if the customer was not told about it properly.

Even though this article is about complaints, prevention matters too. Understanding what is a credit broker before you submit your details can help you avoid a bad experience in the first place. Check whether the firm is authorised, read the fee wording slowly, look for consent language about passing details to third parties, and keep screenshots of the application journey.

Some search terms are awkward, such as how to apply for what is a credit broker, but the real issue behind that phrase is usually how broker led applications work. In practice, you apply through the broker’s journey, but the lender makes the actual credit decision. If that process is not explained clearly, that may itself become part of your complaint.

The same applies to people searching for the best what is a credit broker options. Usually, they are not looking for a definition alone. They are looking for a broker that is transparent about fees, clear about being a broker rather than a lender, and easy to contact if something goes wrong. The safest option is normally an authorised firm with a straightforward complaints route and clearly disclosed terms. You can also use GOV.UK’s guide to complaining about a financial service if you want a simple overview of the complaint path, and Resolver’s credit broking complaints page if you want a tool to organise your complaint and keep records in one place.

Yes. The Financial Ombudsman specifically notes complaints where customers were charged by a broker even though they did not take out a loan or did not receive a suitable offer.

Yes, in most cases. You should give the business the chance to resolve the complaint first. If you are unhappy with its final response, or it does not reply within eight weeks, you can usually escalate.

For most complaints, firms should provide their written outcome within eight weeks.

Yes. You can look the firm up on the Financial Services Register before or after making a complaint.

Raising a complaint about a credit broker in the UK is usually more straightforward than people expect. Start by gathering evidence, complain directly to the broker in writing, and be clear about what you want them to do. If the response is poor, delayed, or unfair, the Financial Ombudsman Service can often review the case for free.

Most importantly, do not let confusion over what is a credit broker stop you from acting. Whether the issue is an unexpected fee, unclear wording, misuse of your details, or a broker presenting itself like a lender, there is a clear complaint route available. Acting quickly, keeping records, and using the formal process gives you the best chance of a fair result.

Complete our quick and easy application form today and see how Result Loans can help you get the right solution for your needs.

Start your application now →